Volatility Crush Provided Relief, but Risk Remains

The S&P 500 has rebounded more than 8% from its year-to-date lows as ceasefire hopes have begun to filter into the market. However, it is not just optimism that has fueled this relatively swift recovery; the move has also been driven by market mechanics.

Volatility, as measured by the VIX, remained above the 20 level for 10 consecutive weeks, a unique occurrence that has only happened once over the past year, during what many referred to as the “Tariff Tantrum” of 2025. This prolonged period of elevated volatility coincided with a pronounced put/call skew in both index options and mega-cap equities, with positioning heavily tilted toward the downside. Traders were paying substantial premiums to hedge portfolios or express bearish views.

But, as with most things in markets, rebalancing was eventually warranted. With even a modest improvement in the news flow, we have begun to see that bearish put skew start to unwind. As traders close out bearish positions, dealers are forced to reposition their own books, often by buying back futures contracts to rebalance gamma and volatility exposure.

This type of repositioning can create sharp and sometimes violent market swings, while also adding momentum to bullish moves. In other words, part of this rally has been driven by a volatility crush and systematic positioning reset rather than purely fundamental improvement.

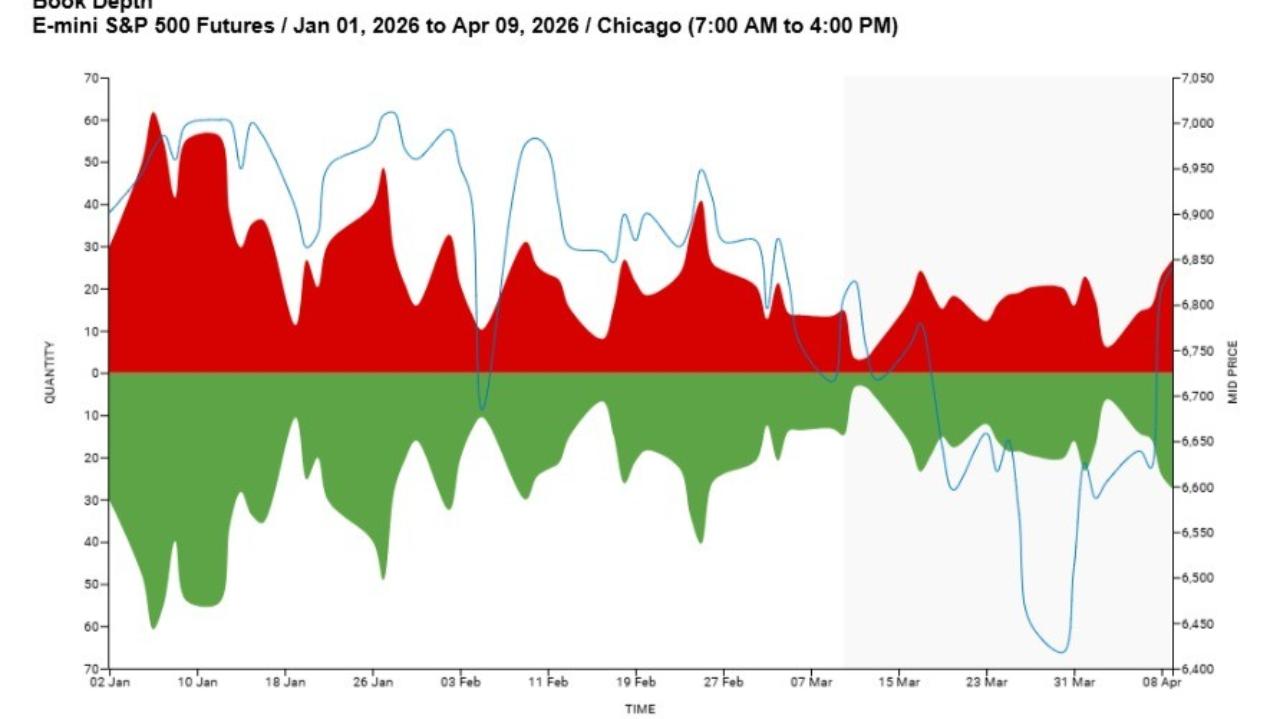

Liquidity has also improved. The CME liquidity tool is showing an increase in book depth, that is, the number of contracts resting on the bid and ask, which tends to have a direct relationship with volatility. Greater book depth generally helps dampen volatility, although liquidity conditions still have room to improve further.

Once again, the conditions were in place for the market to reset positioning, but that does not necessarily mean volatility is behind us. As we head into the weekend, ceasefire negotiations will continue to drive headlines, and markets can reprice risk very quickly.

It is also important to note that earnings season begins Monday, with Goldman Sachs (GS) reporting before the equity open. Earnings could begin to shift investor focus away from geopolitical developments and back toward other perceived risk areas in the market, including the health of the private credit market and the ongoing question of software “cannibalization” driven by A.I.

Featured Clips